Request A Call Back *

Entrepreneurs Guide to Audit of a Company

Private Limited Company, One Person Company and Limited Company registered under the Companies Act, whether publicly or privately held and whether having share capital or not are required to maintain proper book of accounts and get the books of accounts audited each year. In this article, we look at all aspects of audit of a Company.

Appointing the First Auditor of the Company

All types of companies, except a Government company are required to appoint an Auditor within 30 days of date of incorporation of the Company. The Board of Directors of the Company is responsible for the appointment by conducting a meeting of the Board of Directors.

In case the Board of Directors of the Company does not appoint the first Auditor(s) of the Company within 30 days of incorporation of the Company, then the shareholders/members of the Company can appoint the first Auditors of the Company by conducting an extraordinary general meeting.

Power and Duties of Auditor of the Company

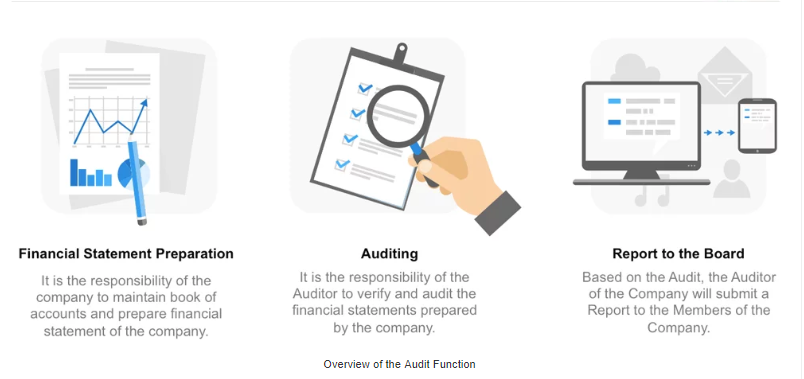

An Auditor of the Company must be an independent person engaged by the Company for the purpose of expressing an opinion on whether the financial statements prepared by the company are free of material misstatements, fraud or error and inline with the Accounting Standards. It is important to note that it is the responsibility of the Company to maintain book of accounts and prepare financial statements of the Company. The Auditor of the Company cannot maintain the Book of Accounts of the Company or prepare financial statements of the Company, as it would impair his/her independence.

The Auditor of a company has the right to access the books of account and vouchers of the company, and has the power to call for any information or documents that is required for performing the duties of Auditor. Further, the Auditor of the Company is mandatorily required to inquire into the following matters:

- Whether loans and advances made by the company on the basis of security have been properly secured and whether the terms on which they have been made are prejudicial to the interests of the company or its members;

- Whether transactions of the company which are represented merely by book entries are prejudicial to the interests of the company;

- Where the company not being an investment company or a banking company, whether so much of the assets of the company as consist of shares, debentures and other securities have been sold at a price less than that at which they were purchased by the company;

- Whether loans and advances made by the company have been shown as deposits;

- Whether personal expenses have been charged to revenue account;

- Where it is stated in the books and documents of the company that any shares have been allotted for cash, whether cash has actually been received in respect of such allotment, and if no cash has actually been so received, whether the position as stated in the account books and the balance sheet is correct, regular and not misleading:

Audit Report for Company

Based on the Audit of the Company, the auditor will make a report to the members of the company stating whether to the best of his/her information and knowledge, the accounts of the company an financial statements give a true and fair view of the state of the company’s affairs. Further, the audit report must also include:

- Whether he/she (Auditor) has sought and obtained all the information and explanations which to the best of his knowledge and belief were necessary for the purpose of his audit and if not, the details thereof and the effect of such information on the financial statements;

- Whether, in his/her (Auditor) opinion, proper books of account as required by law have been kept by the company so far as appears from his examination of those books and proper returns adequate for the purposes of his audit have been received from branches not visited by him;

- Whether the report on the accounts of any branch office of the company audited by a person other than the company’s auditor has been sent to him/her (Auditor).

- Whether the company’s balance sheet and profit and loss account dealt with in the report are in agreement with the books of account and returns;

- Whether, in his/her (Auditor) opinion, the financial statements comply with the accounting standards;

- The observations or comments of the auditors on financial transactions or matters which have any adverse effect on the functioning of the company;

- Whether any director is disqualified from being appointed as a director;

- Any qualification, reservation or adverse remark relating to the maintenance of accounts and other matters connected therewith;

- Whether the company has adequate internal financial controls system in place and the operating effectiveness of such controls;

Restrictions on Statutory Auditors

The Auditors of a Company can only provide services which are approved by the Board of Director or Audit Committee of the Company. Further, under any case, the Auditor of a Company is prohibited from providing the following services “directly or indirectly” to the Company or its holding company or subsidiary company to maintain independence of the Auditor:

- Accounting or Book Keeping Services

- Internal Audit

- Design and implementation of Financial Information System

- Actuarial Services

- Investment Advisory Services

- Investment Banking Services

- Rendering of Outsourced Financial Services

- Management Services.

OUR MISSION

We help Entrepreneurs start and operate successful businesses

Constitutionalcounsels.in is India’s largest online business services platform dedicated to helping people easily start and manage their business, at an affordable cost. Our aim is to help the entrepreneur on the legal and regulatory requirements, and be a partner throughout the business lifecycle, offering support at every stage to ensure the business remains compliant and continually growing.

Constitutionalcounsels.in partners with a network of experienced Chartered Accountants, Company Secretaries, Lawyers, Cost Accountants, Chartered Engineers, Ex-Bankers and Financial Experts across India to provide a comprehensive range of services for small and medium sized enterprises.